Copyright@http://lchipo.blogspot.com/

Follow us on facebook: https://www.facebook.com/LCH-Trading-Signal-103388431222067/

Follow us on facebook: https://www.facebook.com/LCH-Trading-Signal-103388431222067/

***Important***Blogger is not wrote any recommendation & suggestion. All is personal opinion and reader should take their own risk in investment decision.

Open to apply: 13/12/2022

Close to apply: 19/12/2022

Balloting: 21/12/2022

Listing date: 03/01/2023

Close to apply: 19/12/2022

Balloting: 21/12/2022

Listing date: 03/01/2023

Share Capital

Market cap: 168mil (will depend on final IPO price)

Total Shares: 560mil shares

Industry CARG (2017-2021)

Wooden industrial packaging industry, Malaysia, 2017- 2021: CAGR 5.11%

Industrial packaging industry, Vietnam, 2017-2021e: 19.52%

Competitors comparision (PAT%)

L&P group: 11.85%

ETH Holdings Sdn Bhd: 2.32%

Transpak Worldwide Sdn. Bhd: 6.06%

EPE Packaging (Penang) Sdn Bhd: 0.98%

LHT Holdings Limited (its subsidairy): 9.99% (PE6.85)

Nefab (Malaysia) Sdn Bhd: 9.41%

TimberTech Pallet Systems Sdn Bhd: -0.98%

Market cap: 168mil (will depend on final IPO price)

Total Shares: 560mil shares

Industry CARG (2017-2021)

Wooden industrial packaging industry, Malaysia, 2017- 2021: CAGR 5.11%

Industrial packaging industry, Vietnam, 2017-2021e: 19.52%

Competitors comparision (PAT%)

L&P group: 11.85%

ETH Holdings Sdn Bhd: 2.32%

Transpak Worldwide Sdn. Bhd: 6.06%

EPE Packaging (Penang) Sdn Bhd: 0.98%

LHT Holdings Limited (its subsidairy): 9.99% (PE6.85)

Nefab (Malaysia) Sdn Bhd: 9.41%

TimberTech Pallet Systems Sdn Bhd: -0.98%

Business (FYE 2022)

Design and manufacture of integrated wooden based industrial packaging solutions.

Boxes, crates & packing services: 69.97%

Pallets: 27.03%

Provision of circular supply services: 0.85%

Trading as value added sevice: 2.15%

Revenue by Geo

M’sia: 81.39%

Vietnam: 18.61%

Design and manufacture of integrated wooden based industrial packaging solutions.

Boxes, crates & packing services: 69.97%

Pallets: 27.03%

Provision of circular supply services: 0.85%

Trading as value added sevice: 2.15%

Revenue by Geo

M’sia: 81.39%

Vietnam: 18.61%

Fundamental

1.Market: Ace Market

2.Price: RM0.30

3.P/E: 11.72 @ RM0.0256

4.ROE(Pro Forma III): 18.46%

5.ROE: 36.09%(FYE2021), 35.34%(FYE2020), 23.96%(FYE2019)

6.NA after IPO: RM0.13

7.Total debt to current asset after IPO: 0.704 (Debt: 61.656mil, Non-Current Asset: 47.819mil, Current asset: 87.578mil)

8.Dividend policy: proposed 20%-50% PAT dividend policy.

9. Shariah starus: Yes

1.Market: Ace Market

2.Price: RM0.30

3.P/E: 11.72 @ RM0.0256

4.ROE(Pro Forma III): 18.46%

5.ROE: 36.09%(FYE2021), 35.34%(FYE2020), 23.96%(FYE2019)

6.NA after IPO: RM0.13

7.Total debt to current asset after IPO: 0.704 (Debt: 61.656mil, Non-Current Asset: 47.819mil, Current asset: 87.578mil)

8.Dividend policy: proposed 20%-50% PAT dividend policy.

9. Shariah starus: Yes

Past Financial Performance (Revenue, Earning Per shares, PAT%)

2022 (FYE 30Jul, 7mths): RM83.824 mil (Eps: 0.0142),PAT: 9.47%

2021 (FYE 31Dec): RM120.924 mil (Eps: 0.0256),PAT: 11.85%

2020 (FYE 31Dec): RM88.305 mil (Eps: 0.0176),PAT: 11.16%

2019 (FYE 31Dec): RM66.304 mil (Eps: 0.0078),PAT: 6.63%

Profit before tax vs cash from operating

2022: 49.61%

2021: 50.46%

2020: 41.30%

2019: 14.79%

2022: 49.61%

2021: 50.46%

2020: 41.30%

2019: 14.79%

Major customer (2022)

1. First Solar Group of Companies: 55.39%

2. Jinko Solar Group of Companies: 12.12%

3. Customer A: 4.9%

4. Celestica Electronics (M) Sdn Bhd: 3.11%

5. Flextronics Group of Companies: 2.19%

***total 77.71%

Major Sharesholders

B Pack Holdngs Sdn Bhd: 64.51% (direct)

Ooi Lay Pheng: 64.51% (indirect)

Lee Soon Swee: 64.51% (indirect)

Ooi Hooi Kiang: 4.7% (indirect)

Ooi Kah Hong: 4.7% (indirect)

Moviente: 4.7% (direct)

Directors & Key Management Remuneration for FYE2023 (from Revenue & other income 2022)

Total director remuneration: RM0.843mil

key management remuneration: RM0.95mil – RM1.2mil

total (max): RM2.043 mil or 11.93%

Use of funds

1. Capital expenditure: 29.5%

2. Business expansion: 5.9%

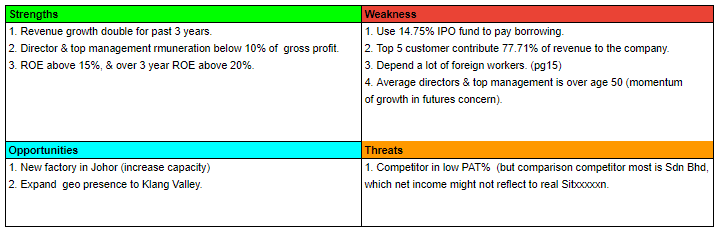

3. Repayment of borrowings: 14.75%

4. Working capital: 38.35%

5. Listing Expenses: 11.50%

1. Capital expenditure: 29.5%

2. Business expansion: 5.9%

3. Repayment of borrowings: 14.75%

4. Working capital: 38.35%

5. Listing Expenses: 11.50%

Conclusions (Blogger is not wrote any recommendation & suggestion. All is personal opinion and reader should take their own risk in investment decision)

Overall is a fair IPO. The company have opportunities to growth when it finish set-up the Johor factory.

Overall is a fair IPO. The company have opportunities to growth when it finish set-up the Johor factory.

*Valuation is only personal opinion & view. Perception & forecast will change if any new quarter result release. Reader take their own risk & should do own homework to follow up every quarter result to adjust forecast of fundamental value of the company.