European and US equity futures rose while a gauge of Asian stocks inched closer to a bull market as investors weighed a slowdown in inflation ahead of the Federal Reserve’s policy decision.

Shares in Hong Kong, Japan and Australia held advances, nudging the MSCI Asia Pacific index toward a three-month high and a close of 19% above its October low.

Futures for the S&P 500 rose about 0.3% in Asia after the US benchmark closed off its intraday peak on Tuesday. Investors are awaiting more clues on the Fed’s interest-rate path from the decision later Wednesday and Chair Jerome Powell’s briefing.

The dollar traded little changed after losing ground to its Group-of-10 counterparts the previous session. The New Zealand dollar fell in a decline that accelerated after the government warned a recession was likely next year.

Treasuries added to their rally on Tuesday, when data showed Powell’s key measure of services prices excluding energy and rents moderated again in November. While price pressures appear to have peaked, headline CPI remains above 7%, suggesting the Fed has more work to do to rein in inflation.

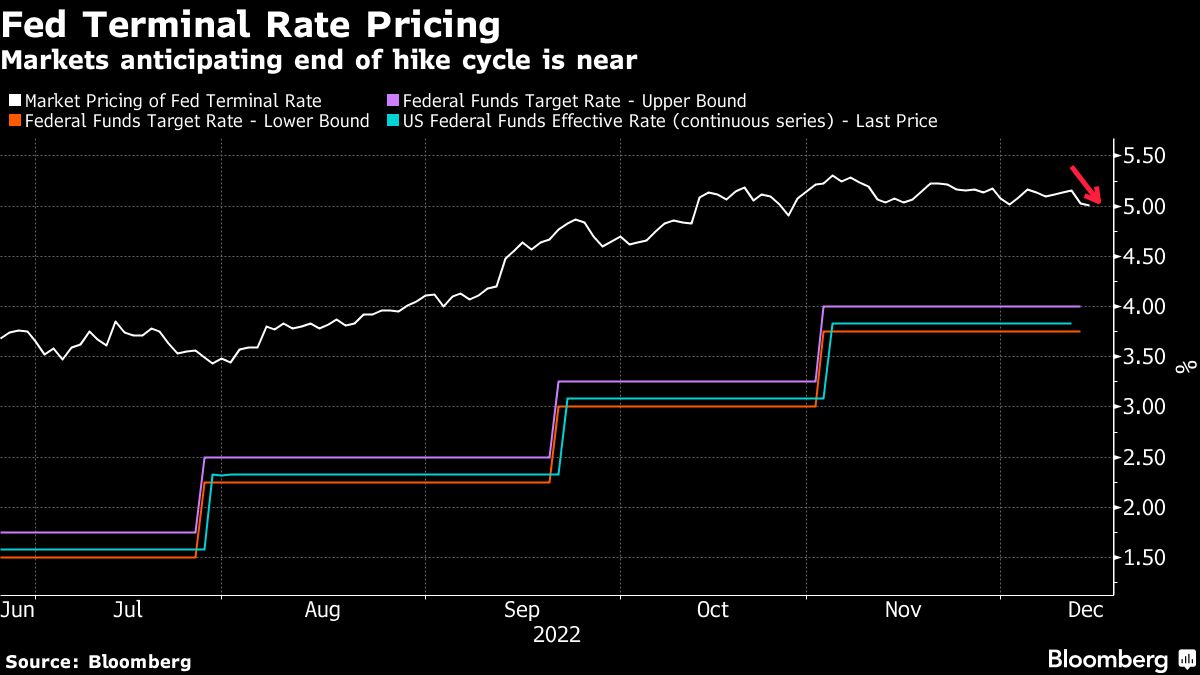

“The market is now anticipating a slower pace of hikes and a moderation of the peak terminal rate in the US,” said Kellie Wood, deputy head of fixed-income at Schroders in Sydney. “We believe the market is fully priced for this interest rate cycle given the level of inflation in the US economy.”

A dovish repricing swept across rates markets on Tuesday. With a half-percentage point move by the Fed notched in, wagers leaned toward a quarter-point increase as early as February. Further out, swaps priced the peak Fed policy rate around 4.85% by May, down from almost 5% ahead of Tuesday’s inflation print. The current Fed policy range is 3.75% to 4%.

Elsewhere in markets, Bitcoin held near the one-month high reached on Tuesday in a sign of investor appetite for risk taking.

Oil fell slightly ahead of the Fed decision and after rallying 6% over the previous two sessions. Gold steadied near its highest level since July.

The price of iron ore fell for a third day as traders attempted to plot the effects of China’s shift away from pandemic restrictions and a rise in Covid infections.

Following the Fed, the European Central Bank will announce its rate decision Thursday. Markets will also contend with decisions from the Bank of England and monetary authorities in Mexico, Norway, the Philippines, Switzerland and Taiwan.

Key events this week:

- FOMC rate decision and Fed Chair news conference, Wednesday

- China medium-term lending, property investment, retail sales, industrial production, surveyed jobless, Thursday

- ECB rate decision and ECB President Lagarde briefing, Thursday

- Rate decisions for UK BOE, Mexico, Norway, Philippines, Switzerland, Taiwan, Thursday

- US cross-border investment, business inventories, empire manufacturing, retail sales, initial jobless claims, industrial production, Thursday

- Eurozone S&P Global PMI, CPI, Friday

Some of the main moves in markets:

Stocks

- Futures on the S&P 500 rose 0.3% as of 6:42 a.m. London time. The S&P 500 gained 0.7%

- Nasdaq 100 futures climbed 0.3%. The Nasdaq 100 climbed 1.1%

- The Hang Seng Index rose 0.7%

- The Topix index climbed 0.6%

- The Shanghai Composite Index fell 0.1%

- Euro Stoxx 50 futures rose 0.1%

Currencies

- The Bloomberg Dollar Spot Index fell 0.1%

- The euro was little changed at $1.0638

- The Japanese yen rose 0.1% to 135.43 per dollar

- The offshore yuan was little changed at 6.9616 per dollar

- The British pound was little changed at $1.2371

Cryptocurrencies

- Bitcoin was little changed at $17,768.28

- Ether was little changed at $1,319.38

Bonds

- The yield on 10-year Treasuries declined two basis points to 3.48%

- Japan’s 10-year yield was little changed at 0.25%

- Australia’s 10-year yield declined three basis points to 3.36%

Commodities

- West Texas Intermediate crude fell 0.4% to $75.11 a barrel

- Spot gold was little changed

© 2022 Bloomberg