Updated in October 2023.

In the dynamic world of eCommerce, stagnation is not an option. As digital storefronts become the norm and consumer preferences shift at lightning speed, understanding and adopting the latest payment trends is paramount. It’s not just about facilitating a transaction; it’s about enhancing the entire shopping experience.

For businesses looking to grow, keeping a finger on the pulse of payment innovations is a necessity. Strap in as we explore the global payment trends set to shape 2024 and beyond.

Online Payment Trends

Online payments have undergone a massive transformation in recent years. Let’s unpack the major online payment trends that are redefining the eCommerce landscape.

Contactless payments take center stage

NFC (Near Field Communication) has been embedded in some credit cards since 2007 in the UK, but today more than 80% of credit and debit cards have built-in contactless.

Of course contactless is significantly faster and easier than chip-and-pin, but the main reason for its popularity is the mobile wallet. The likes of Apple Pay, Google Pay and Samsung Pay allow consumers to make purchases with the one device that’s almost always on their person—their phone.

With the ability to hold multiple debit & credit cards, plus solutions like PayPal, mobile wallets has revolutionized the payment experience for consumers.

Contactless as a response to Covid-19

Once Covid-19 was known to transmit through surfaces, the desire for contactless as a safe payment method skyrocketed. Many businesses and retailers quickly adapted by upgrading their payment systems to accept contactless payments, driving even wider adoption from consumers. In Italy, contactless usage went up by 83%, while in Germany, it rose by 42%.

Covid was a major trigger for increased spending limits through contactless. Transactions were initially limited to small amounts, but several countries in Europe have now set €100 limits (or higher) on contactless spending. In the United States, there is no limit at all.

This behavioral shift is expected to have lasting implications for the payment industry, with contactless payments likely to remain a dominant payment method in the post-pandemic world.

Embrace alternative payment methods

The exponential rise in convenience isn’t limited to contactless payments. A revolution has also begun in embedded finance, a solution where businesses take payments directly inside their platform or app. For example:

- Ride-sharing apps offering in-app wallets

- eCommerce platforms providing instant loans

- Social media platforms enabling peer-to-peer payments

Supporting a range of alternative payment methods is a crucial differentiator in the digital age. The ability of non-financial companies to offer financial services creates a more seamless user experience.

Another example is the Buy Now, Pay Later (BNPL) phenomenon. Where staggered payments used to be the hallmark of credit institutions, now virtually any online seller can offer installments or deferred payments.

While appealing, BNPL does create risk for both parties. For companies, cash is king and overreliance on deferred payments is never comfortable. But for consumers, the ease of accruing debt, interest and late fees is staggering. The effects on long-term financial stability and credit scores can be damaging. There is a lot to consider before offering, or accepting, a BNPL plan.

Enhanced security and biometric authentication

The rise in contactless and embedded payment solutions is accompanied by increased attention to security and regulations, as the convenience of these methods can be exploited; in the United States, where there are no contactless payment limits, stolen smartphones or phished login details can lead to unauthorized purchases until reported.

Biometric authentication, such as fingerprint readers in smartphones, offers higher security and ease of use compared to traditional methods like passwords or PINs, gaining popularity among consumers, and paving the way for gradual acceptance of facial recognition, despite some initial challenges.

Localization will be more critical than ever

The online payment landscape for international sellers has become diverse. Each region has distinct preferences. Credit cards remain dominant in North and South America, but in Europe payment wallets (like PayPal) are extremely popular. According to the Baymard Institute, 6% of US shoppers abandon their cart if their preferred payment method is unavailable.

Something we all have in common is the desire to pay in our local currency. It is a competitive disadvantage to refuse local payment methods. But the payment ecosystem is dynamic. New payment methods emerge and old ones evolve. Staying updated with these changes is essential for businesses to remain relevant.

For brands looking at global expansion, localized payments are a crucial pillar for a brilliant customer experience.

Bonus: Discover these actionable tactics to maximize your profits by recovering abandoned carts on your online store.

Cryptocurrency and digital assets

Cryptocurrency may not have seized traditional banking, but it is gaining traction as a viable payment option, especially Bitcoin and Ethereum. There is a growing market of consumers and vendors who champion the decentralized nature of cryptocurrency. Giants like Microsoft, Tesla and Whole Foods already accept cryptocurrencies; eCommerce is likely to follow.

In theory, cryptocurrencies offer superior security, lower transaction fees and are totally borderless. While these factors are hugely appealing to global brands, the challenges—like their rampant volatility and evolving regulation—make imminent adoption on a mass scale unlikely.

Offline Payment Trends

Offline and in-person payments are constantly evolving with technology and consumer expectations. Increasingly, the line between on and offline is blurred. Let’s look at the key trends that are shaping the future of offline payments.

Smart POS systems and integration

The evolution of traditional POS systems into smart, connected devices has revolutionized the retail industry. Beyond processing payments and printing receipts, smart POS terminals have touchscreens, internet connectivity and the ability to run third-party apps. They’re more secure and have a versatility that works with everything from retail to hospitality.

Integrating offline and online data is by far the most powerful benefit of smart POS systems. Brands can track the customer journey across channels; they can make data-driven decisions and optimize inventory management, marketing and sales.

While POS systems are ostensibly offline products, they are being catapulted into the digital age and are giving brick-and-mortar businesses the opportunity to scale their online activity more easily.

QR code payments

QR codes owe their massive resurgence to the Covid-19 pandemic. One area QR codes dominated was hospitality: they became the go-to method of sharing both menus and payment options for restaurants and bars. Customers scan the code, browse the mobile site, place their order and put their feet up.

QR codes are simple, brands can create them for free and get creative with their implementation. But while most aspects of daily life have returned to normal, QR codes have stuck around. They remain particularly popular for person-to-person payments: simply scan the code to launch PayPal or Venmo, with all the payment information instantly generated. Gone are the days of slowly inputting bank details for manual transfers.

While QR codes need testing and can be finicky to set up, they run well and make life extremely easy for consumers. Far from a fleeting trend, the QR codes are only becoming more popular.

Real-time payments

The world will never go back to the days of slow payments. Real-time payments supercharge cash flow, allow brands to instantly send payment confirmations (which builds trust) and can be conducted across the globe. It is probably the single biggest innovation in modern banking.

As always, the true demand for real-time payments comes from consumers. As they become more accustomed to instantaneous services in other areas of their lives, they expect the same when making purchases.

The growth of real-time payments can be attributed to technological advancements and innovations in the payment sector. Modern infrastructure and systems have made it possible to process payments in real-time, and both consumers and businesses have grasped the opportunity with both hands.

Like QR codes, the value of real-time payments is not limited to any sector or industry. They are being used for everything from peer-to-peer transfers to major business transactions. And when everyone gets paid faster, it has a strong and positive effect downstream. Advancements will come thick and fast as more investment is made in the technology.

Voice-activated payments

While voice-activated assistants are seen as gimmicks by many, they have become immensely popular. The likes of Amazon’s Alexa, Google Assistant, and Apple’s Siri integrate with phones, smart homes, speakers and even cars. And now users can initiate transfers, check account balances and even make purchases just by speaking to their device.

This hands-free approach is being leveraged by all sorts of consumers and is especially beneficial for visually impaired individuals or those who find traditional payment methods cumbersome. It also offers a new channel for sales & engagement for brands.

But unsurprisingly, there are major security concerns.

Voice recognition is nowhere near as robust as biometric sensors or the PIN code. Systems can easily misinterpret commands and voices can be mimicked. How exactly the industry will overcome these vulnerabilities is unknown. End-to-end encryption, multi-factor authentication, and continuous monitoring for suspicious activities will be crucial.

Downstream from security concerns is the issue of adoption: most people do not like experiments when it comes to their money. Users need near-absolute assurance that their money is safe and that the technology is reliable. Until that is provided, voice-activated payments will continue in the small minority of payment methods.

Sustainable and green payment solutions

While the payments industry is taking strides towards sustainability, it’s hard to see their efforts as much more than token gestures. Payment cards from sustainable materials are nice, but offered by a tiny number of paid accounts.

Digital receipts are the other big-hitter in sustainable payments. While the eradication of paper receipts is welcome (and long overdue) adoption is limited. The primary benefit of digital receipts is probably ease for the consumer, rather than environmental conscience.

Carbon offsetting is another opportunity for payment companies to influence change. For example, a portion of transaction fees can be directed towards environmental projects like planting trees, supporting renewable energy projects or other carbon offset programs. This is a genuinely positive step that will hopefully be taken by many more payment companies in the coming years.

What The Experts Recommend

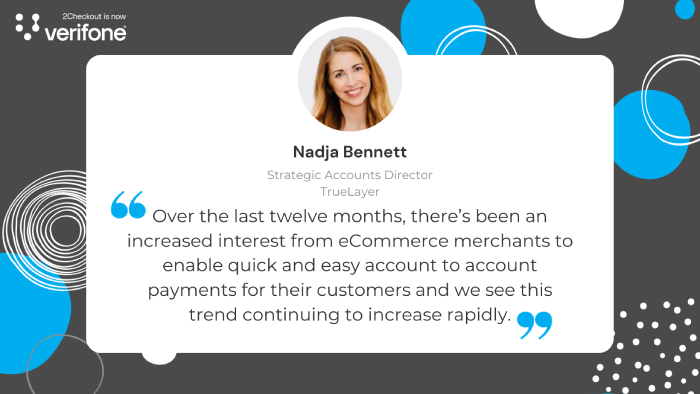

Nadja Bennett, Strategic Accounts Director at TrueLayer:

“Following the introduction of SCA in the UK and Europe, merchants are looking at ways to improve the checkout experience without having to jump through hoops of exemptions, to keep the flow as frictionless as possible all whilst keeping fraud, chargebacks and costs at a minimum. Enter Open Banking! Over the last twelve months, there’s been an increased interest from Ecommerce merchants to enable quick and easy account to account payments for their customers and we see this trend continuing to increase rapidly in 2023. Learn more about the rise of open banking payments in the UK in this report.”

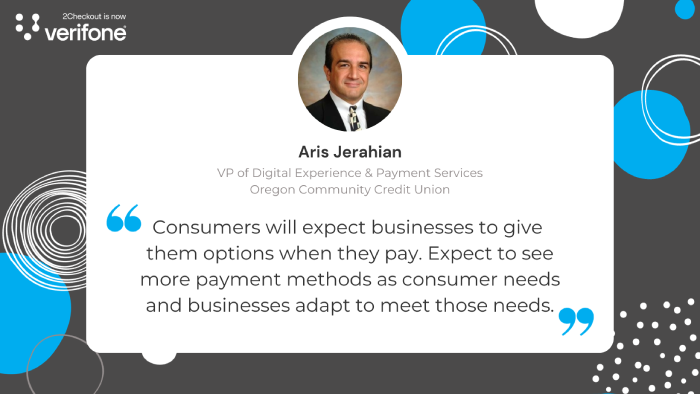

Aris Jerahian, VP of Digital Experience & Payment Services at Oregon Community Credit Union

“During 2023 eCommerce payment trends will revolve around providing a better, safer shopping experience. Consumers are returning to in-person shopping, but they won’t give up on the convenience of digital payments. Pandemic behavior is here to stay as consumers have no choice but to use digital payment methods. The checkout process has become the most important part of a sales journey.

Digital wallet options are now a common fixture alongside other traditional payment options and merchants need to get on board. Same as QR codes – once they seemed to die out, only to come back with a vengeance. Today it’s used as menus, forms of payment, tickets, receipts, etc.

Consumers will expect businesses to give them options when they pay. Expect to see more payment methods as consumer needs and businesses adapt to meet those needs.”

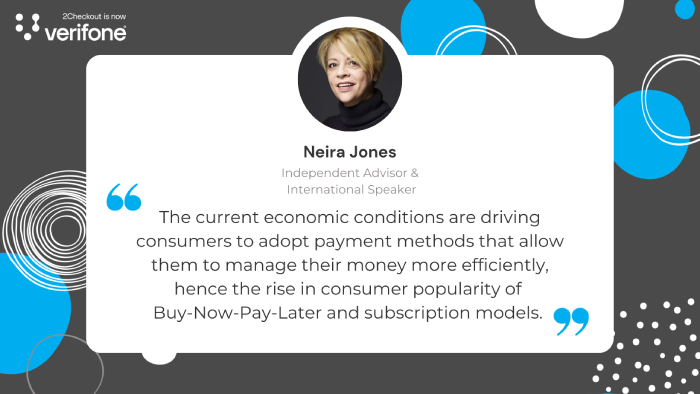

Neira Jones, Independent Advisor & International Speaker, Neira Jones

“Over the last few years the payments industry has become increasingly digital. The current pandemic has served to accelerate that trend exponentially, with both businesses and consumers adopting digital payments faster than they would otherwise have done. The current economic conditions are also driving consumers to adopt payment methods that allow them to manage their money more efficiently, hence the rise in consumer popularity of Buy-Now-Pay-Later and subscription models. For businesses, Open Banking and real-time payments will increase in popularity as cash flow is an increasing challenge. As a result, digital B2B payments can only increase in adoption, and challenger banks and other new entrants are well set to help.”

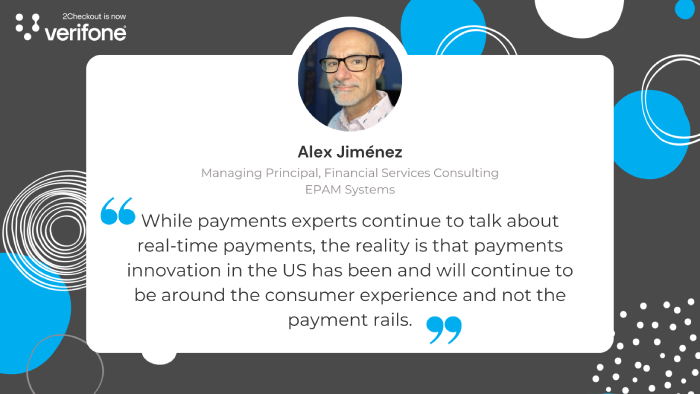

Alex Jiménez, Managing Principal, Financial Services Consulting at EPAM Systems

“While payments experts continue to talk about real-time payments, the reality is that payments innovation in the US has been and will continue to be around the consumer experience and not the payment rails. COVID has accelerated the adoption of digital payments schemes by forcing more people to try embedded experiences, such as DoorDash or Postmates, and by moving to contactless payments including digital wallets and contactless cards. Additionally, P2P adoption is also growing particularly by small businesses who have resisted digital payments prior.

The pandemic economy is driving up higher use of debit cards, same as the method behind digital payments, as people are spending more on non-discretionary items and foregoing discretionary items. Credit card use will stall, while Buy Now, Pay Later (BNPL) schemes gain more users. There is a renewed interest in daily payroll solutions offered by fintech firms, such as DailyPay. At the same time, issuers are tightening underwriting standards for credit cards. The move to more digital payments, also means an increase in digital fraud.”

Glenn Geil, EVP – Head of North American Payments Delivery, at Endava

“Endava has been a driver of RTP and Open Banking in Europe for many years. From this deep history and having lived through how they can come together for a powerful payment experience, we believe that Consumer to Merchant payments via RTP and Open Banking (often referred to as Open Payments) are set to become a powerful trend in US payments. The costs of card interchange, once viewed as a default cost of sales, are now a painful margin killer that needs a solution, and Open Payments can be that solution.

We believe that it will take off first in the eComm space as businesses and PSP’s can integrate it similar to other alternative payment methods. On the consumer side, the world of wallets and stored payment credentials will limit the friction of switching to an Open Payments method.

FedNow’s July launch has brought the price point of RTP to consumer usage levels, and the recent announcement by Early Warning Services about their common bank wallet opens the door for future RTP merchant payments to be initiated right from the banking app, where many consumers go first to check their balance prior to a transaction.

The benefits to the eComm business are absolutely worth the cost to integrate. The catch is enticing the consumer to switch from the card to a direct bank transfer. One challenge is for those with loyalty cards. A business will need to come up with a replacement value add, as there must be some incentive to give up the points, but that value-add should preserve as much of the interchange savings as possible.

The bigger challenge is making the consumer feel equally capable of disputing fraud and errors, as that has become the safety net with using cards. The issue will not be the handling of actual disputes, but more the consumer fear of what would happen once they lose their “card-given rights.” For this reason, we believe that businesses catering to the delivery of software, services, and the subscription delivery of goods could be the first to benefit, as trust in the delivery is significantly higher in these areas. Once non-card dispute practices start to normalize, the use of RTP and Open Payments will spread more rapidly to the remaining areas of eComm.”

This RTP/Open Payments trend will start to roll out later in the year, but businesses should start planning now for how to telegraph to their client base the dispute assurance and loyalty incentives that will entice them to make the switch.”

Don Cardinal, Managing Director, Financial Data Exchange

“The Financial Data Exchange (FDX) is unifying the financial industry around a secure, interoperable and royalty-free standard for consumer-permissioned data sharing. In the payments space, we see trends for increased focus on privacy, security, and inclusivity – both from consumers and regulators. We believe that global best-in-class authentication schemes like FAPI, which FDX leverages, will continue to see adoption and use. In the same way, we see increased interest and adoption of interoperable standards in payments because they lower the barriers to entry and level the playing field for small firms as well as new entrants into the market led by under-represented groups.”

Conclusion:

As we approach 2024, the global payment landscape is in the midst of a transformative shift driven by technological advancements, changing consumer preferences, and the aftermath of global events like the Covid-19 pandemic. This article has delved deep into several key trends that are set to shape the future of payments:

- Contactless Payments & Mobile Wallets

- Embedded Finance & BNPL

- Enhanced Security & Biometric Authentication

- QR Code Payments

- Real-Time Payments

- Voice-Activated Payments

- Sustainable & Green Payment Solutions

- Smart POS Systems

For eCommerce businesses, these trends underscore the importance of adaptability. The future belongs to those who can swiftly incorporate these trends and exceed customer expectations. It’s not just about offering a service; it’s about enhancing the user experience, ensuring security, and being socially responsible.

In this ever-evolving landscape, platforms like 2Checkout (now Verifone) play a pivotal role. We provide businesses with the tools and insights needed to navigate these changes, ensuring they remain at the forefront of payment innovation. As we move forward, partnering with 2Checkout (now Verifone) could be crucial for your business to thrive in the dynamic world of global payments.