Options – the hottest ticket in town

In the 4th Quarter of 2023, for the first time, the daily volume of Options traded in the US eclipsed the daily volume of Futures traded. Options are now the #2 product behind Stocks by volume.

There are two particular phenomena drawing our attention – Zero Day Options and Option Strategies embedded in Mutual Funds and ETFs.

Some investors might want to get just a rudimentary understanding of Options and recent products, while others might want a deeper dive. I have written two columns.

In this month’s column, we’ll take up three major topics:

- An introduction to options and their role in the market

- The market’s latest passion; so-called Zero Day Options, a mania in the US and India, and

- Options embedded in the fund and ETF strategies.

Next month, I’ll dive deeper into a few Options funds and related analyses of their performance and associated risks.

Our Introduction to Options

The simplest possible explanation

In the normal course of events, investors who want to change the risk profile of their portfolios can do one of two things. They can sell something they own or they can buy something they don’t. Easy.

But what if you’re a nervous investor who is not yet ready, or able, to sell part of their portfolio? What if you’re a bullish investor who is not yet ready, or able, to buy more for their portfolio?

Options offer a third path. They are structured financial products that for a price offer you the opportunity but not the obligation to act. You might nervously own shares at $38 but suspect that they might end up at $28. You could address your anxiety by going to an options broker to buy the opportunity (i.e., the option) to sell your shares at $35 at any point in the next three weeks. If they do fall below $35, you’re saved! If the shares don’t fall, you’re out the amount of your payment to the broker.

With me so far? You need to negotiate a price target ($35 in our example), an expiration (after three weeks), and a premium (the amount the broker will charge you). The same process applies if you think some security is going to climb in price and you’d like the opportunity to benefit from its rise.

For investors who are long stocks, anxious options are called “put options.” Greedy options are called “call options.”

Fifty Shades of Options

The options market we know today turned 50 years old last year. Modern options markets took off when Myron Scholes and Fischer Black published the Black-Scholes formula for options pricing in 1973. The Chicago Board of Trade set up the Chicago Board Options Exchange in ’73. In 1974 AMEX and CBOE set up a clearing system for options transactions, kicking off the options industry.

Options became popular with investors in the dot com boom, but have shown their dominance only over the last few years.

Why am I writing about options?

First, investors are enamored with options. Positively besotted. I wonder how much investors understand options, but I do know investors dearly love options.

Money has been flowing toward these funds in an unrelenting torrent. Morningstar’s vice president/research (and esteemed curmudgeon) John Rekenthaler writes:

It’s no secret that actively managed stock funds are on the outs. Counting both mutual funds and exchange-traded funds, they suffered $43 billion in net outflows in December 2022, $34 billion the previous month, and $31 billion the month before that. After a while, as the saying goes, such losses can become real money.

Covered-call funds, however, have attracted $65 billion in net inflows over the past three years. Through every month of that period, their net sales have been positive. (“Covered-Call Stock Funds Like JEPI Are Popular. Should They Be?” 1/24/2024)

The second reason I’m writing about options is that an MFO reader reached out to us and asked whether we thought such funds were something they should consider. This one’s for you, Kapil!

The market’s latest passion: Zero-day Options

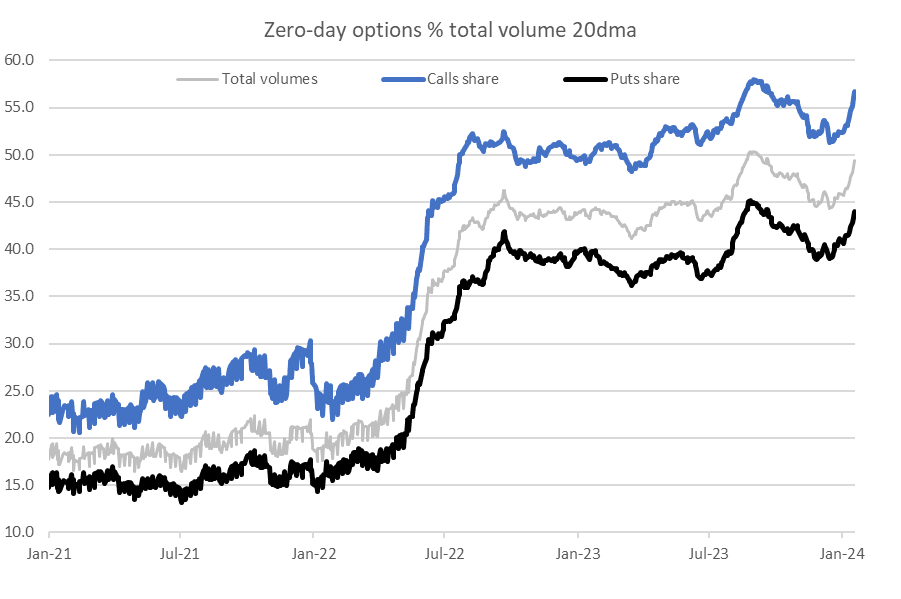

Zero-day options, which are so named because they expire on the same day they are traded, now account for almost half of all daily Options volume. It’s akin to buying house insurance for one day or betting on same-day lotto.

Such options are attractive to a wide variety of folks. For example, speculators looking to trade based on momentum, technical analysis, and news flow. Or, professional traders looking to manage their risks around macroeconomic data or events.

A recent chart from the WSJ ( source Citibank):

Despite the fascination of same-day options, American options traders are a boring bunch compared to options traders in India.

In a Feb 26th, 2024 column, A tale of two bull markets, fund manager, author, and FT columnist Ruchir Sharma writes:

Most bull markets see excesses build up over time; in India, they are visible in subsets of the growing retail investor class. In 2023, Indians purchased more than 85bn options, or nearly eight times the volume in the US, and on average held those contracts for less than half an hour. Amid the frenzy, regulators ordered trading platforms to open with a warning that 90 per cent of retail investors are losing money on these trades. (Italics emphasis are mine).

When the holding period of an investment comes down to thirty minutes, we know that whoever is doing it, is having a lot of fun. This can’t be about financial planning. This is about getting rich yesterday.

Zero-day options do offer sharp shooter institutional customers and hedge funds a way to manage their stop losses on levered bets. Such short-term options are useful for speculators and hedgers, but they are not important to long-term buy and hold investors of stocks and bonds.

Lessons from The California Gold Rush

Perhaps the best I can do is to remind you of an interesting historical parallel.

The California Gold Rush created vast fortunes, just not among the gold prospectors. The people who made huge gains were the intermediaries, the guys who sold stuff to the prospectors. While the prospectors braved violence, hunger, life-threatening weather, disease, and failed mines, the merchants and hoteliers stayed in comfortable homes and let the money trickle in steadily for years. You surely know the story of Levi Strauss, whose Levi Strauss & Co. denims were wildly popular, and profitable, but do you know the guy who was vastly richer than Strauss? Samuel Brannan became the richest man in California and its first millionaire by selling as much as $5,000 worth of goods a day – maybe $150,000 in current dollars – to gold miners. He ended up buying much of the Napa Valley.

The California Gold Rush created vast fortunes, just not among the gold prospectors. The people who made huge gains were the intermediaries, the guys who sold stuff to the prospectors. While the prospectors braved violence, hunger, life-threatening weather, disease, and failed mines, the merchants and hoteliers stayed in comfortable homes and let the money trickle in steadily for years. You surely know the story of Levi Strauss, whose Levi Strauss & Co. denims were wildly popular, and profitable, but do you know the guy who was vastly richer than Strauss? Samuel Brannan became the richest man in California and its first millionaire by selling as much as $5,000 worth of goods a day – maybe $150,000 in current dollars – to gold miners. He ended up buying much of the Napa Valley.

The others in that coterie of ultra-rich – William Randolph Hearst’s father among them – thrived by keeping their hands clean and their cash registers full. The winning formula?

During a gold rush, sell shovels.

The same lesson applies here, dear readers. Retail investors who buy and sell options are – on the whole, over time – going to lose money. The only reliable winners in the options game are the same people who reliably win in casinos: the dealers. The wealth of casino magnates is built on the simple premise that “the House always wins” because whether you, individually, win or lose a particular bet makes no difference to them.

Why Options hold an important place on Wall Street

- Linear vs Non-Linear Payoffs: An option is akin to a lottery ticket while a stock is like a house. A fully paid house won’t go up or down in value over a day, a month, or even a year. But winning a jackpot can change my life. Options are the closest that retail investors get to non-linear payoffs. Retail is willing to invest time, money, and a portion of their portfolio in options. In this, they are mirroring the institutional investors who have long used options to juice portfolio returns judiciously. It remains to be seen if either institutions or retail can consistently use options to make money. No one breaks out their portfolio attribution from stocks vs options.

- Commissions: at most online trading shops, there is zero commission for trading stocks and ETFs. But options are not commission-free. Incentives are important.

- Options Education: Because options are far more complicated than stocks (and also more profitable), an enormous amount of educational tools are available online. Retail traders are investing time and energy in learning how to become options smart.

- Options Exchanges: In the late 1990s, all the exchanges: the CBOE, the CME, and the NYSE, were private and owned by the brokers who owned the seats at the exchange. Since then, exchanges have been demutualized and are now publicly traded enterprises. They are big businesses that benefit from volumes in futures and options. Following are four big US exchanges, their equity market capitalization, and their last 12-months profits.

-

- CME: $75 Billion ($3.05 Billion in profit)

- NYSE’s owner Intercontinental Exchange: $73 Billion ($2.4 Billion)

- Nasdaq: $34 Billion ($1.1 Billion)

- CBOE: $19 Billion ($709 million)

We needed the Black-Scholes, the options exchanges, the bull market in stocks, options education, market-makers, and the desire on the part of investors to be options-educated and embrace risk to arrive at a place where options are now traded more than futures (but less than stocks).

Options-based strategies in mutual funds and ETFs

The other important movement in Options is the flow of assets into fund strategies involving options.

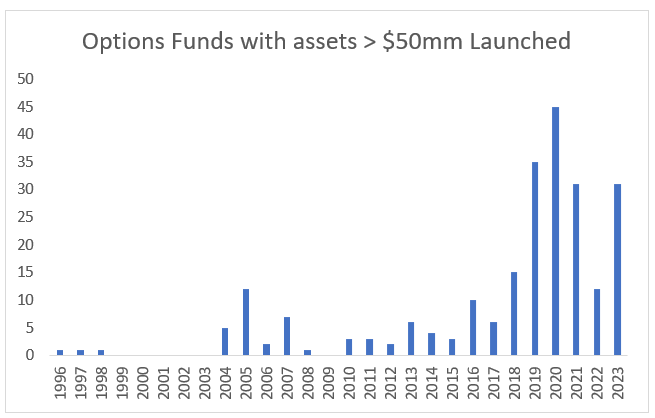

A search in Ycharts for funds with more than $50mm in Assets, categorized as Derivative Income or Options Trading yielded 238 funds with an asset base of $181 Billion. The median fee on these funds is about 0.85% per year or a total fee income of $1.2 Billion annually. The chart below splits these 238 funds by year of inception.

The oldest of these funds (Shelton Equity Income Investor) launched 28 years ago but the vast majority have just a few years of operation. The biggest name in Options-related funds today is JP Morgan.

$76 Billion of the approx. $181 bn in options funds AUM are parked in nine JP Morgan funds. Here are the top three Options linked funds in the market and they are all JP Morgan funds.

- JP Morgan Equity Premium Income ETF (JEPI): $32.6 Bn AUM

- JP Morgan Hedged Equity (JHEQX): $17.7 Bln

- JP Morgan Nasdaq Equity Premium Income ETF (JEPQ): $10.7 Bln

Options funds usually engage in some combination of the following three strategies:

- Buy write: they buy stocks/index and overwrite with call options to collect option premium income. These funds have high distribution yields (about 6-8%).

- Put write: these funds sell puts collateralized by cash and hope to pocket the premium from underwriting puts.

- Buffered (Hedged) Notes: these funds buy and hold stocks/Index and use combinations of Puts and Calls to hedge the equity holdings.

Each fund may have a different proposal for what they intend to hold as equity risk: S&P 500 Index, Nasdaq, International Stocks, or Emerging Market Stocks

Each fund may have a different proposal for how they intend to use options to either earn Derivative Income by a. and b. above or create a Hedged Equity fund for c. above.

While some funds may be fairly programmatic in their choice of underlying stocks/index, and how they use options, it’s best to think of every options-related fund as an Active fund. They certainly charge fees in the magnitude of 0.8% per year, which is in line with active equity funds. The trading around of options and stocks generates plenty of short-term capital gains (and losses) which again is symptomatic of active funds.

Why do Options and Stocks as a combination work in Hedged Equity funds?

Investors are used to 60/40 allocation funds which hold a portfolio of stocks and bonds. In such funds, bonds act as an indirect hedge, appreciating when stocks sink. There is no guarantee that bonds will work when stocks don’t. 2022 and 1st three quarters of 2023 proved that balanced portfolios did not balance. When the bond indirect hedge does work, it requires a specific set of economic or interest rate conditions to be met (low inflation, slowing growth, Federal Reserve interest cuts, etc).

On the other hand, options can be a direct hedge. Owning a diversified US equity market portfolio, either through the S&P Index or one of the large-cap funds focused on growth or value, can be efficiently hedged through Options structures. Similarly, selling options generates income. And some marketers have equated options income to bond income. They are not the same kind of income.

Bond income comes from interest and rent. Selling options is to underwrite a part of the future distribution of a stock or an index. I might sell a put 50% lower than the current price of the stock and make pennies every month of the year betting the stock will not crash. That’s a different kind of income than one that comes from lending money to a company (a bond).

Option structures have been experimented with for decades on Wall Street with institutional customers. They are now just coming to retail investors. Each option structure (or options fund) needs a specific version of the future path of market returns to be most effective. Along with the innovation, also comes the fees, the complexity, the education involved, and the difficulty of choosing which fund to buy.

What’s the most logical case for ordinary investors to consider Options-related funds?

Some investors want to or need to be invested in stocks. Stocks have run up a lot. Even though it looks like they are still the place to be, stocks can go down by a third to a half. We experienced that during March 2020 Covid and then in 2022-2023. Some investors are willing to give up some equities in return for partial protection on the downside. This to me is the most logical case for investing in an options fund.

There are so many of them. By my crude estimate, there are over 150 funds with close to 90 Billion dollars of hedged equity funds. How should one decide what to buy? Biggest? Oldest? Highest return? This is not easy work. I hope to show one way to analyze these funds in next month’s column. The upshot is just like there’s only a handful of actively managed equity and bond funds one should be invested in, the same applies to options funds. And that is if we squint really hard in making a case for such funds.

In Conclusion

The forces that have come together over the last fifty years in popularizing options are getting bigger and stronger. It’s important to objectively consider investor needs and the stickiness of their needs – hedged or income solutions – in determining if the funds will reverse flows. The flows are here to stay. We should be aware of the trends and familiarize ourselves with the analysis required to determine if a fund is worth our money.

The guiding principles of financial planning and long-term investments are unchanged. For those who can stick to the discipline, no amount of options cleverness is a substitute for a strong and stable financial foundation.

Media Links: Devesh’s YouTube Videos on Derivatives History & Financial Times Article

A few years ago, I was highly motivated to run a YouTube channel and recorded videos on various asset classes. I made a playlist titled, (A few) People’s Story of Equity Derivatives in the USA. There are 10 videos which run from 1972 to 2004. Those looking to learn about how the options market became as big as it has will find a lot of fertile information in those videos. I no longer add videos to the channel.

Robin Wigglesworth of the Financial Times did an excellent interview with Sandy Rattray and me (ex-Goldman Sachs VIX inventors) and my friend, John Hiatt (Chicago Board Options Exchange) on our work for the VIX Index creation, An oral history of the fear index (9/20/2023) on the 20th anniversary of the VIX Index.