What is happening with homebuilders and the new home sales sector as we head into the spring housing market? We have had some conflicting data points recently. On the one hand, cancelation rates have been rising. On the other hand, mortgage rates have gone down more than 1% since Oct. 20, 2022.

The builders’ stock prices have done well as mortgage rates have fallen, and this illustrates the simplicity of the homebuilders’ position: their story is really about mortgage rates and moving products.

The builders sell homes as if they were a commodity: they build and sell to make the most money possible and move on. The builders don’t like to see supply of existing homes growing for fear that their buyers might cancel on them. The growth of supply means demand is getting weaker, which will require builders to give more incentives to buyers.

Now, they want to ensure that the buyers who are still qualified are still there to close the deal when homes are ready to move into. This makes them much more efficient sellers than existing homeowners, who need to find another house once they sell. The builders don’t have that problem — they just want to get homes off their books as soon as possible.

So, as the 10-year yield has fallen along with mortgage rates, investors are anticipating the builders can sell more of their products once they’re ready to be moved into. This is the biggest reason why homebuilder stocks have done so well recently.

How many new homes are out there?

The latest Census report shows that 71,000 new homes are completed and good to go, which is close to the historical average for new homes completed of 80,000 to 100,000.

Here’s the breakout:

- 71,000 new homes have been completed: 1.4 months of supply.

- 291,000 homes are still under construction: 5.7 months of supply

- 99.000 homes have yet to be started: 1.9 months of supply

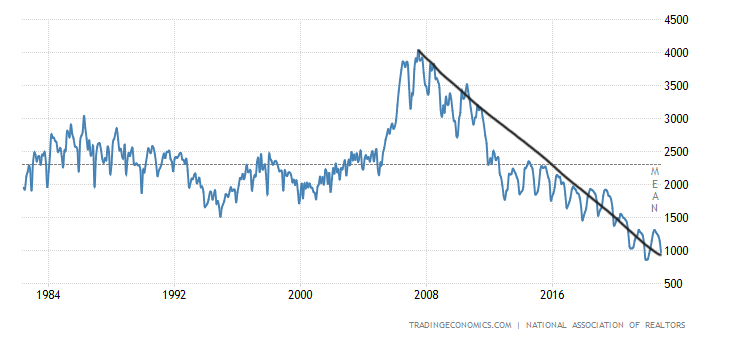

As you can see, this is not a lot of homes when you consider the population of the U.S. The builders actually lucked out here because back in 2007, we had over 4 million active listings of existing home, which are usually cheaper than comparable new homes. Based on the last NAR existing home sales report, we only have 970,000 active listings — this is the second-lowest level ever in recent history going into January.

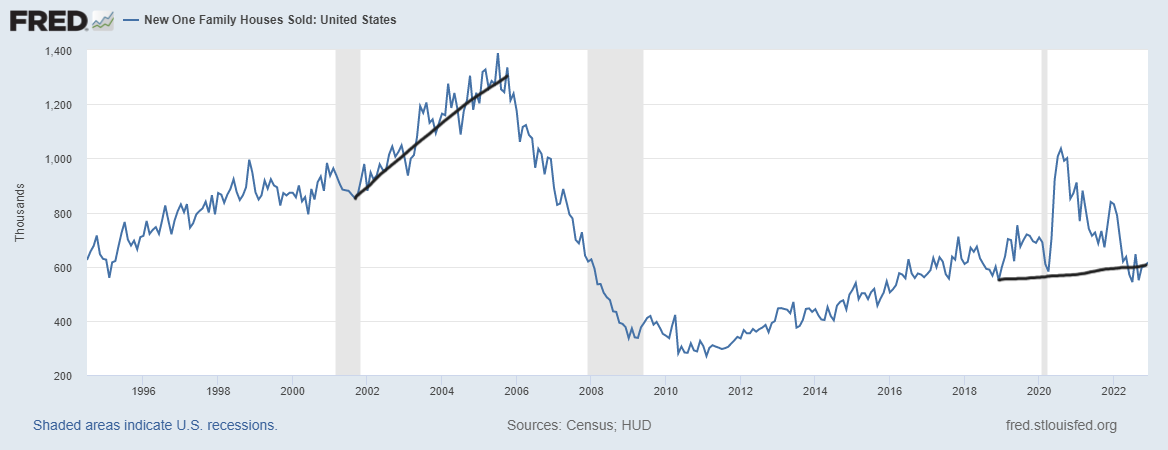

New home sales are still historically low

From Census: New Home Sales Sales of new single-family houses in December 2022 were at a seasonally adjusted annual rate of 616,000, according to estimates released jointly today by the U.S. Census Bureau and the Department of Housing and Urban Development. This is 2.3 percent (±18.5 percent)* above the revised November rate of 602,000, but is 26.6 percent (±13.2 percent) below the December 2021 estimate of 839,000. An estimated 644,000 new homes were sold in 2022. This is 16.4 percent (±3.8 percent) below the 2021 figure of 771,000.

As you can see below, new home sales haven’t gone anywhere for some time now, and the previous months’ data tends to get revised lower. The headline number doesn’t account for cancelation rates. So, in reality, we wont see movement here until mortgage rates get low enough for the cancelation percentage to decline.

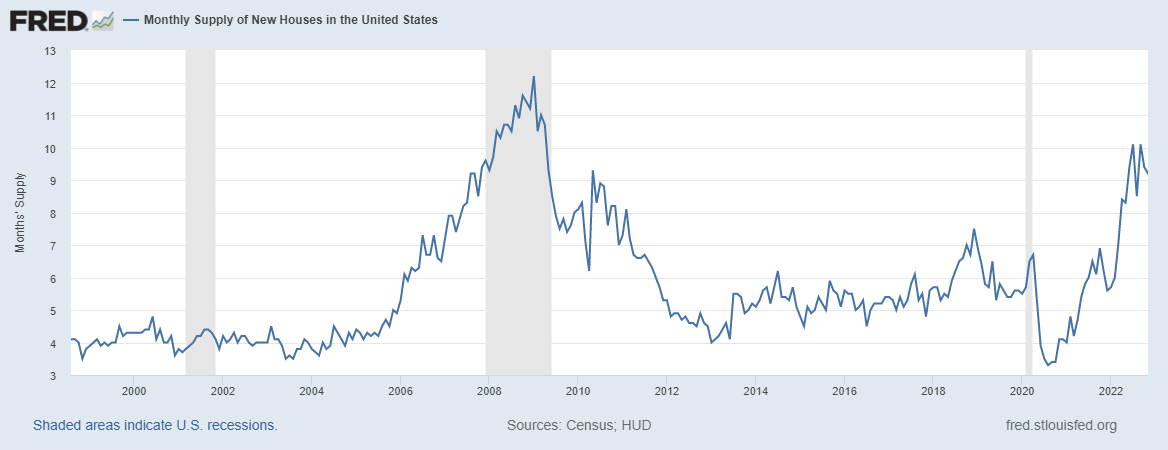

For homebuilders, the monthly supply of new homes is still too high

From Census: For Sale Inventory and Months’ Supply, The seasonally adjusted estimate of new houses for sale at the end of December was 461,000. This represents a supply of 9.0 months at the current sales rate.

The monthly supply for new homes is still too high; this is why housing permits are falling noticeably lately. The builders never want to oversupply a market because that would ruin their business model.

My rule of thumb for anticipating builder behavior is based on the three-month supply average. This has nothing to do with the existing home sales market; this monthly supply data only applies to the new home sales market, and the current 9 months is too high.

- When supply is 4.3 months and below, this is an excellent market for builders.

- When supply is 4.4 to 6.4 months, this is an OK market for the builders. They will build as long as new home sales are growing.

- The builders will pull back on construction when the supply is 6.5 months and above.

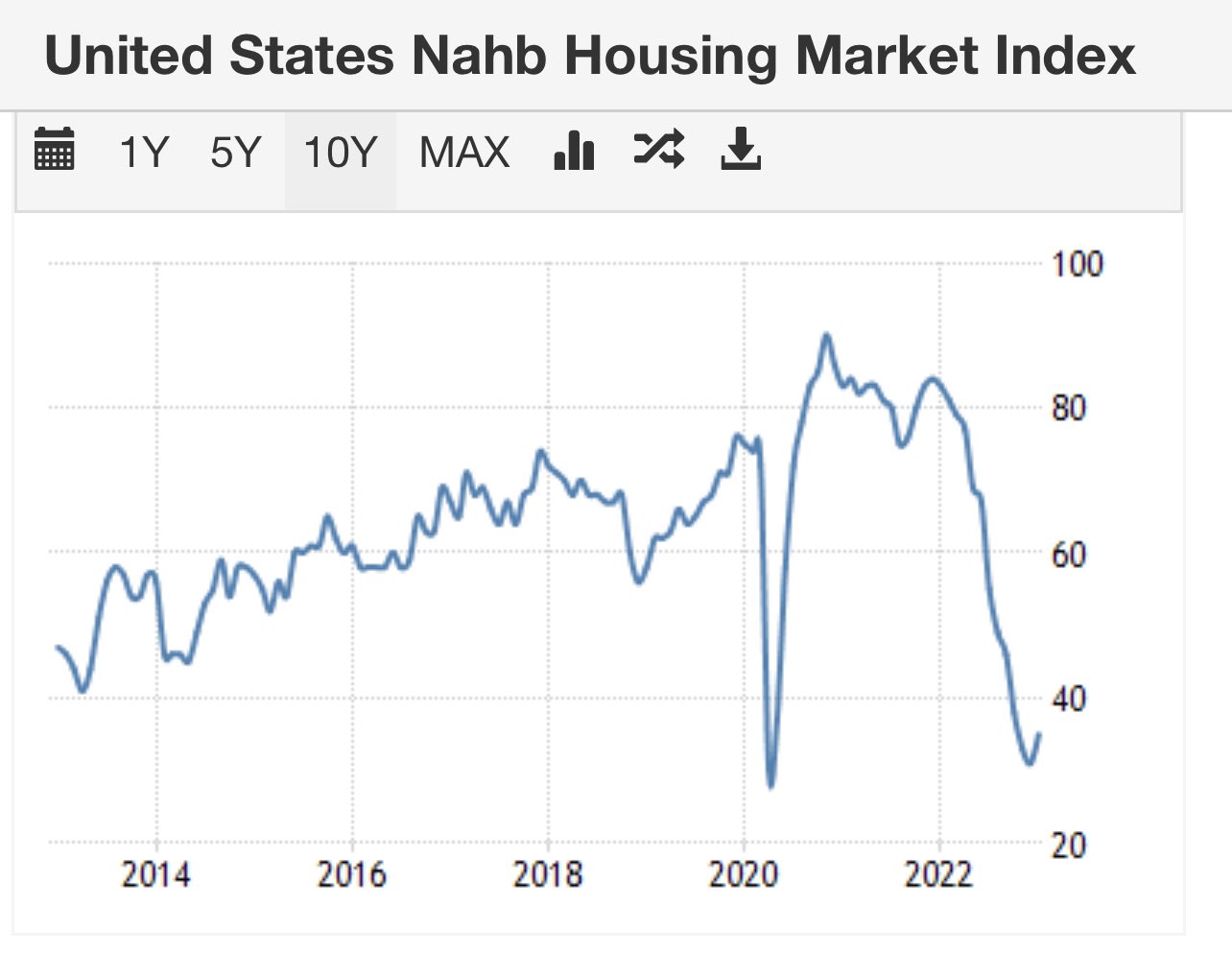

I do understand why certain people, especially 2008 housing crash people, are confused about why the homebuilders’ stocks have rallied so hard recently. But since Oct. 20, mortgage rates have been heading lower, which means bond yields have headed lower. This traditionally means money goes into the builder stocks — they’re not expensive stocks and now have a much better balance sheet, like U.S. homeowner households, as seen in the chart below.

On the economic side of the equation, we still have a lot of work to do here. The builders have to work off the backlog of homes, but instead of 3%-4% mortgage rates, they’re dealing with 6% plus mortgage rates, which means they have to provide many incentives to make sure those homes sell. Since mortgage rates have fallen, the homebuilder confidence index has stopped falling, and we have had an uptick recently. The point I am making here is that it’s about rates now.

As long as bond yields don’t reverse course and mortgage rates don’t go higher, the story should stay the same. However, if mortgage rates can actually get down toward 5%, the homebuilders will be more excited, as this was the level last year that got more buyers into their market. Plus, they might not need to discount so much by then.

However, until that bridge is crossed, the builders will grind this out, finish up their backlog of homes and try to close as many deals as possible.