Dear reader,

Thank you for your question. This is a tricky one – partly because you didn’t provide a lot of information, but also because one cannot compare RAs as they differ from platform to platform and have different underlying funds.

I will answer based on my experience and the industry knowledge I have accumulated over the years.

Firstly, contributions

In many instances we see that the initial monthly contributions were relatively small amounts – R300 to R500 with maybe a 10% annual escalation.

If you had started with R500 per month and an annual escalation of 10%, over a 10-year period, this will have accumulated to around R95 618.

Depending on the funds you invested in, this amount may have grown substantially or it may have decreased.

Fees and commissions

On top of this, one has to factor in the fees.

Older generation products were still hosted on older legacy platforms with extremely high administration fees, [rather than the ‘new age’ open platforms where fees work on a sliding scale.] We have seen annual fees on some of these investments in the region of 7% per annum.

In the past, advisors received their ‘sign up’ commissions and all servicing commissions (based on the term of the retirement annuity they signed) upfront. The investor then ‘repays’ the administrator over the term of the ‘policy’. In other words, from a monthly contribution of R500, say R150 is deducted for ‘repayment’ fees and only R350 is invested. So if you stop your contributions or want to move your investment to another platform before the term maturity date you are ‘penalised’ by a certain amount which equals the outstanding fees that would have been generated had the annuity continued to term.

In all honesty, [some] clients did not understand all these terms and conditions when they initially signed the contracts and now, years later, are shocked when they see how they have performed.

Continuous management and reviewing of investment portfolios is very much needed. Without these, clients are ‘left behind’ when new opportunities arise or when certain sectors are underperforming over multiple periods.

The older generation retirement annuities on the older platforms also have (or had) a limited choice of investment funds and options.

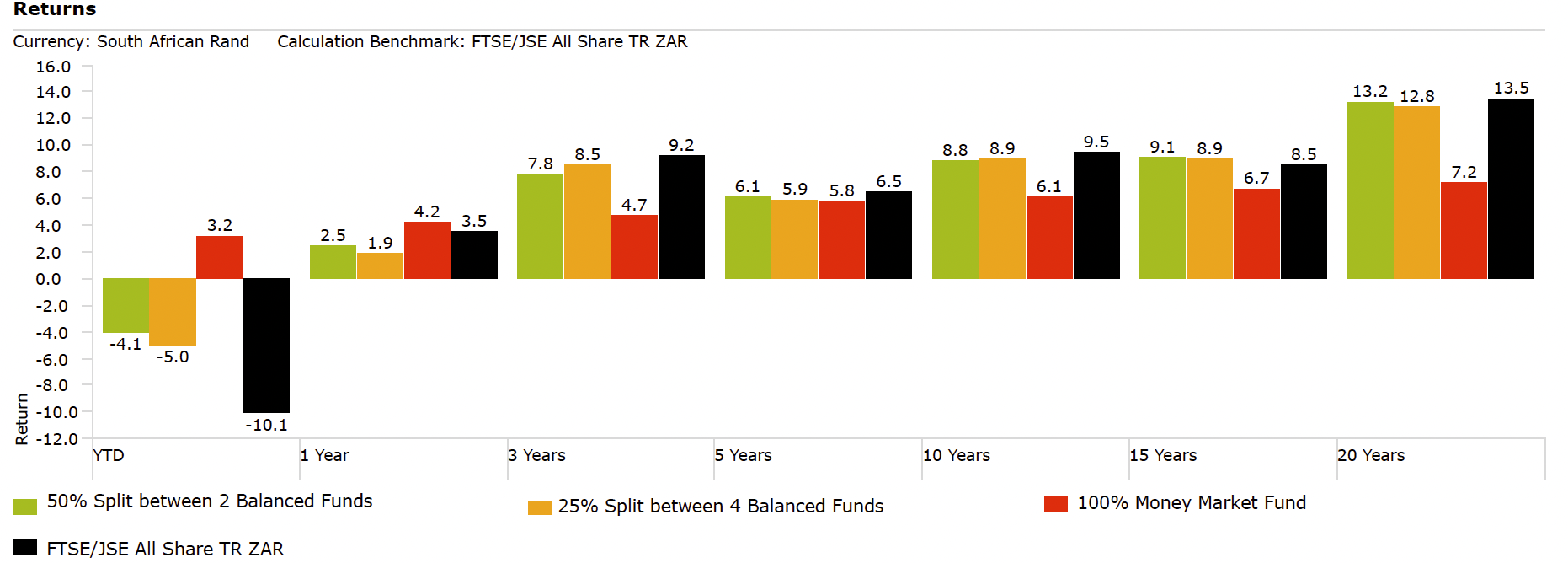

The following graph shows a comparison I did over the last 20 years on different funds and combinations of portfolios:

Source: The author

Another aspect one needs to keep in mind is that in the ‘olden’ days Regulation 28 of the Pension Funds Act, which limits the degree to which retirement funds may invest in certain assets, was not a compliance requirement.

Regulation 28 has now been around for a number of years, and the limit on offshore allowances was increased earlier this year.

Even if the local market has outperformed offshore markets on a year-to-date basis, you have to look at things over the longer term.

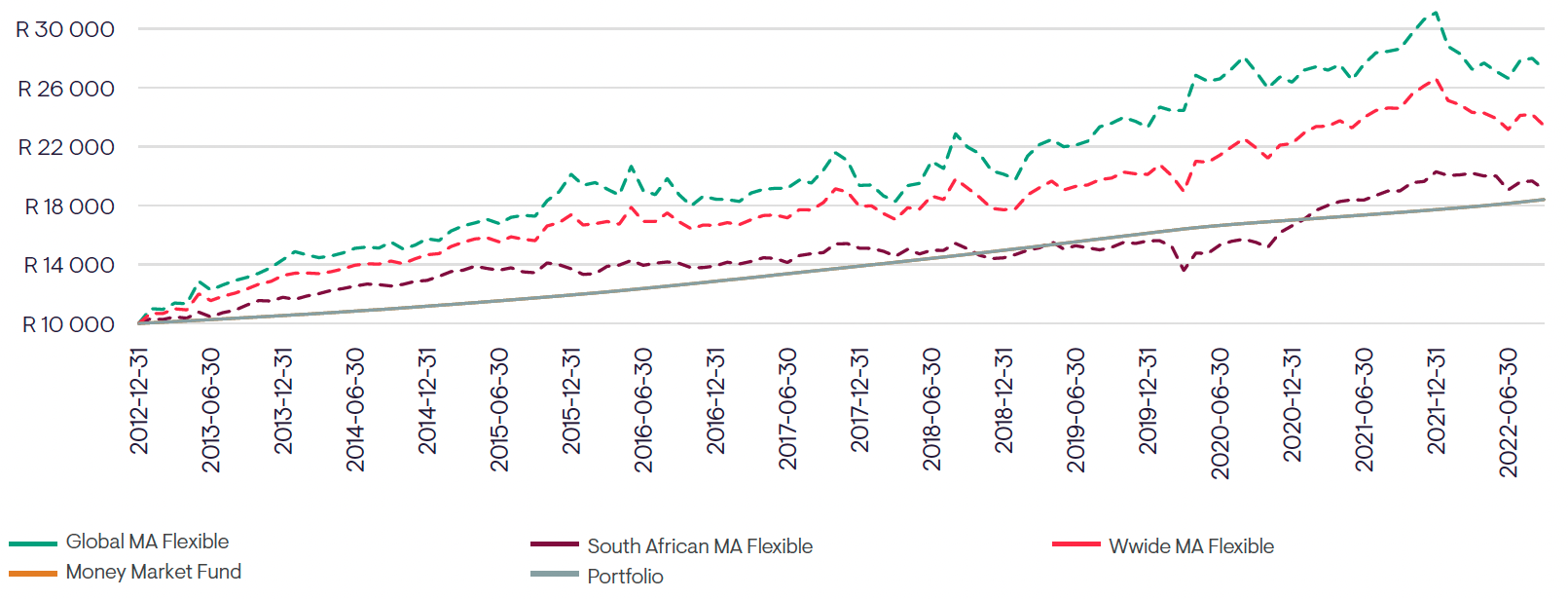

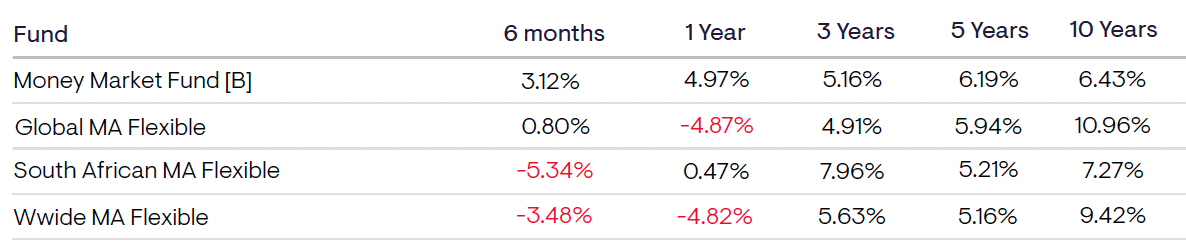

By having sufficient offshore allocation within your investment, you would have benefitted, as can be seen in the following analysis.

Source: The author

Being diversified and managing your portfolio will give you a better opportunity for long-term investment growth.

Being invested in one sector or market will at times give you a greater return, but the risk is also much higher when there is market volatility.

Most – if not all – retirement annuities are transferrable between platforms these days. It is known as a Section 14 transfer and is neutral in terms of fee and tax implications.

The only cost might be the ‘fee repayment’ settlement that is still due to the existing ‘old’ platform. You will only be made aware of this ‘penalty’ once you ask for a Section 14 ‘transfer out’ quote.

I trust that this information helps answer your questions.

As always, it is best to speak to a professional advisor regarding investment matters.