After 13 years of a near-vertical updraft for financial assets, there’s a generation of financial advisors who have never had to explain sequence-of-returns risk to their clients, much less help them make some hard choices about retirement they may never have expected to make.

These advisors are what Catelyn Stark from Game of Thrones would call “the knights of summer.” And winter is coming.

Even Professor Google is underprepared: A search for information about inflation risk yielded 650,000 returns. Longevity risk, 425,000. Duration risk, 113,000. Sequence risk? 32,800.

“The last decade hasn’t done us any favors in this regard,” says Jamie Hopkins, a managing partner of wealth solutions at Carson Group in Omaha, Neb., and a specialist in retirement income planning.

The onset of high inflation for the first time in 40 years triggered a cascade of market events this year, derailing the powerful long-term trends in stock and bond prices. Between January 1, 2009, and September 15, 2022, the Standard & Poor’s 500 produced annualized returns of 13.61%, even after factoring in this year’s nasty bear market (the S&P 500 fell 17.26% for the year through September 15). Bonds, often viewed as a safe haven in bear markets, also succumbed to inflation—the Bloomberg Barclays Aggregate Bond Index fell 12.07% this year through September 15, leaving investors with nowhere to hide.

“All of those first risks fall to the core of investment management strategies,” Hopkins says. “You handle them for all of your clients. Inflation is important for a 22-year-old and an 85-year-old. The challenge with something like sequence risk is that it impacts a much smaller group of clients for maybe three to five years at the beginning of retirement, but it can destroy them on the back end.”

In layman’s terms, sequence-of-returns risk, or sequence risk, is the danger that a market downturn might coincide with a retiree’s first withdrawals from a portfolio, and that those withdrawals will significantly compromise the portfolio’s ability to last through retirement. In 1994, William Bengen authored an article in the Journal of Financial Planning that conceived the popular so-called “4% rule,” which was actually 4.5% in his paper.

Bengen examined how new retirees fared if they started making withdrawals in a variety of historical market scenarios. He found that investors would not outlive their money if they used a 4.5% withdrawal rate from a portfolio evenly divided between stocks and bonds. However, market developments of the past year have prompted a serious reappraisal. Some like Christine Benz, Morningstar’s director of research, advise today’s retirees to lower their withdrawal rates to 3% of their assets, no easy feat for many. Bengen himself has written in Financial Advisor that there is no reason why 4.5%, or any number, should be set in stone.

Sequence-of-returns is still a relatively new concept in the financial advisory glossary. And it took a long time before the financial services industry—so heavily focused on accumulation—took sequence risk seriously enough to develop strategies for mitigating it.

“The retirement income arena inside the financial services industry is only about 20 years old,” Hopkins says. “I started in 2010, and it was not part of the CFP curriculum. It wasn’t until 2016 that the [CFP Board] added retirement income. This is a competency that’s existed only for a few years, and that’s the gold standard of education.”

The reason for the failure of the financial services industry to tackle sequence risk, he says, comes down to the simplest issue: money. “Most of the industry isn’t compensated for managing that risk,” Hopkins says. “In the grand scheme of the industry, it’s not worth it.”

Anthea Perkinson, the founder and principal of Monterey Associates in Pelham, N.Y., agrees.

“That’s exactly right. The average advisor is very conversant in investments and investment returns, less conversant in tax planning, and even less when dealing with clients who go from relying on a paycheck to relying on a portfolio,” she says. “And it’s part of the reason I’m fee-based, and hourly for the most part. My income is not based on assets, where all my attention would go to accumulation.”

The Cost Of Retiring In The Wrong Year

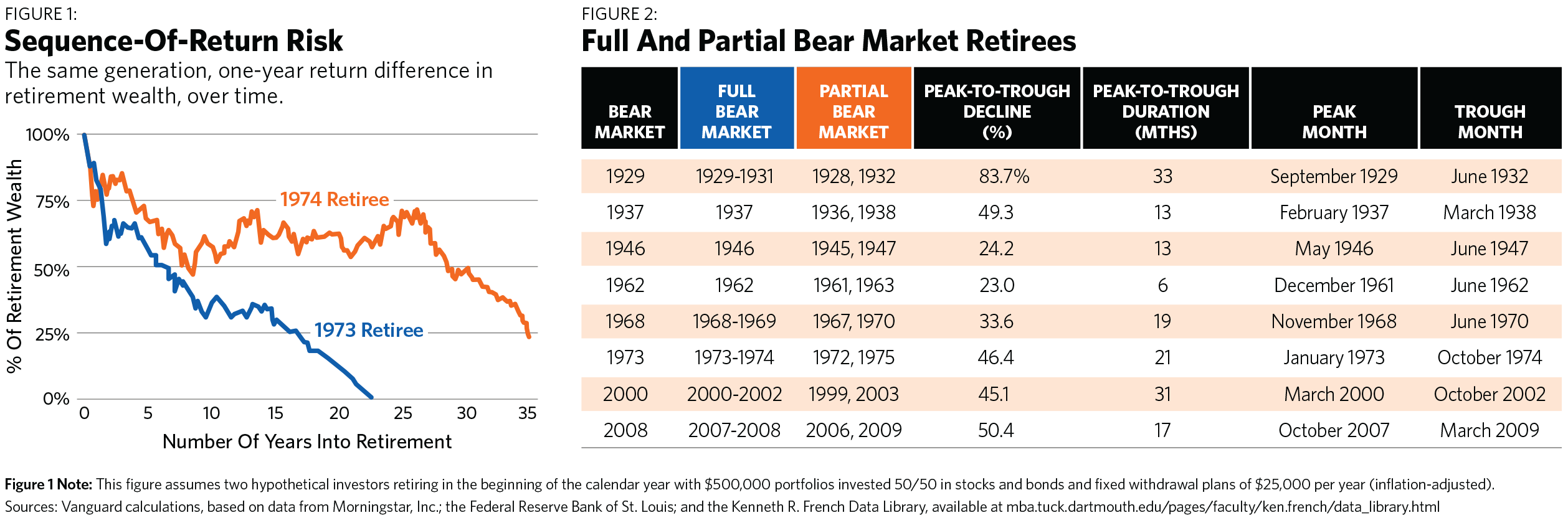

Sequence risk might be short-lived, but it can have long-term implications. To help investors see how it works, a team of researchers at Vanguard Group has published two reports that look at how the problem may play out for today’s retirees.

The first, called “Safeguarding Retirement In A Bear Market,” was released in June 2020 and examined the effect of sequence risk on retirees who depend on a financial portfolio to generate income. Authors Kevin I. Khang and Andrew S. Clarke began their research in 2008 during the global financial crisis and were prompted by the pandemic to release their findings.

“At the start of 2020, we wanted to add more precision to our thinking on the topic of managing sequence risk in the face of bear markets. The Covid-related market selloff hit shortly after, and it sharpened our focus on the topic,” Khang says in an email interview. “We aimed to understand what happened in past bear markets and recessions, assess how big of a difference adverse sequence risk could make in retirees’ well-being, and use that to inform what may be actionable for today’s retirees.”

And so the researchers examined what happened to people who retired during or near six major U.S. bear markets since 1926 and compared them to those who retired in bull markets. Their findings were brutal.

Those unlucky retirees who suffered a poor succession of returns—only because of the timing of their retirement—were 31% more likely to outlive their wealth, had 11% lower retirement income streams and left 37% smaller bequests.

“Every withdrawal turns a negative return, which is temporary in nature, into a permanent impairment of the balance,” the Vanguard team wrote. “The amount withdrawn at a considerable loss reduces the opportunity to recover over the long term. Because the opportunity cost of withdrawing a dollar—measured in the expected return on the dollar until the end of retirement—is particularly high immediately after sequence-of-return risk strikes, the ‘magic’ of compounding return works against the retirees who must do so.”

As an example, they took two hypothetical retirees, one retiring in 1973 and one in 1974. The researchers assumed that, at retirement, the investors’ total wealth was held in balanced portfolios, evenly split between stocks and bonds and rebalanced monthly, and that the portfolios were the retirees’ sole income source for 35 years of retirement. Both employees entered retirement with $500,000 and planned to withdraw $25,000 per year (5%), adjusted for inflation—higher than the popular 4% rule of thumb, but more in line with what advisors tend to see among clients.