Coinbase and Uniswap are two of the leading crypto exchanges. The market values COIN, Coinbase’s stock, and UNI, Uniswap’s token at about 3x trailing 12-month revenues. But should they be trading at similar multiples?

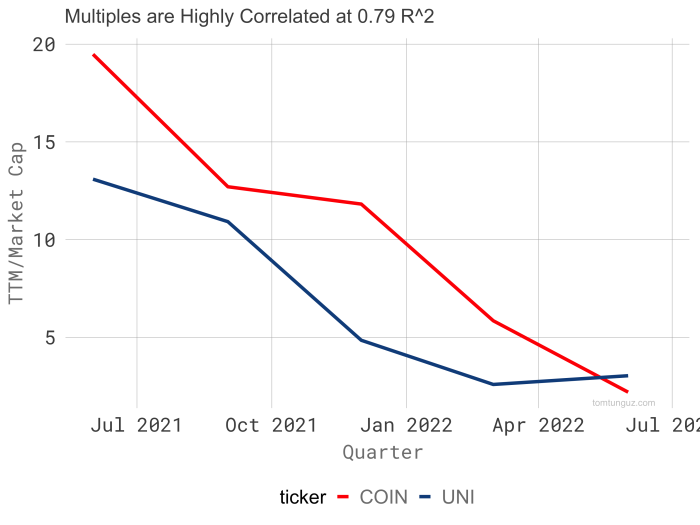

As the market has corrected, so have the trailing 12-month revenues (TTM)/Market Cap multiples. They move in synchrony with an R^2 of 0.79.

Just how comparable are these businesses?

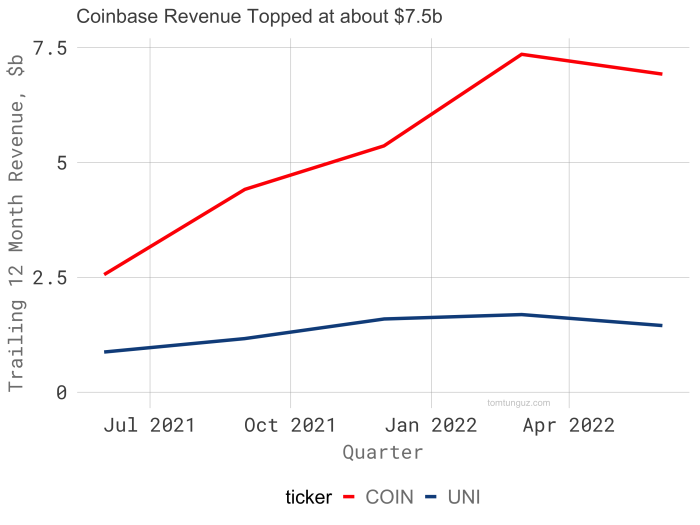

Coinbase and Uniswap generate billions in revenue. Coinbase’s trailing revenue in Q1 2022 approached $7.5b with 34% net income margin (profit). Uniswap recorded $1.7b in revenue in the same period.

Their business models differ meaningfully. Coinbase operates a centralized exchange, while Uniswap runs a decentralized exchange (DEX). Centralized exchanges hold or custody user accounts. DEXes rely on users to custody accounts in wallets.

The difference is starkest in headcount: Coinbase employs more than 5,000 people while Uniswap counts fewer than 100. Consequently, Uniswap generates $14.9m per employee, compared to Coinbase at $1.38m, a 10x difference in efficiency. This implies Uniswap’s net income margin exceeds Coinbase’s (33%) by quite a large margin.

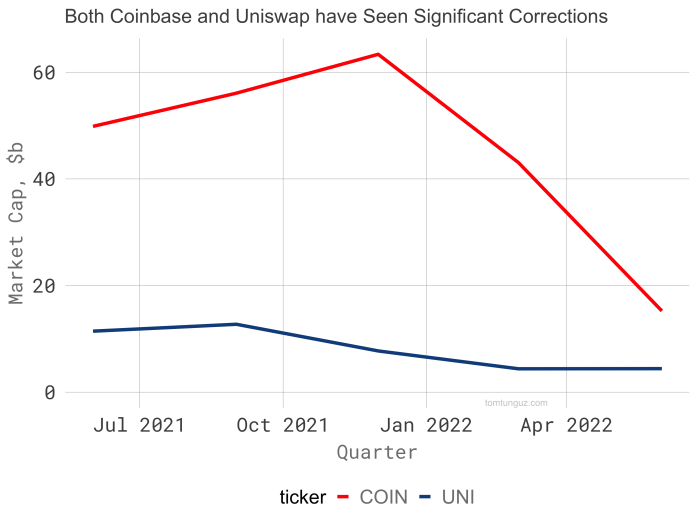

Both UNI and COIN have fallen from their all-time highs recently, suffering from recent revenue declines. During this period, COIN fell 75% from its high compared to UNI’s decline of 65%.

These companies endure the volatility of the crypto summers and winters together. Revenue growth correlates at 0.60.

However, in the last four quarters, Coinbase has outgrown Uniswap, and in the downturn, suffered less revenue decline.

Coinbase counts 4x the number of users as Uniswap. Uniswap monthly transacting users (MTU) grew 366% compared to Coinbase’s growth of 307%.

Uniswap generated 12x the volume per MTU in 2020. In 2021, the gap between the companies narrowed.

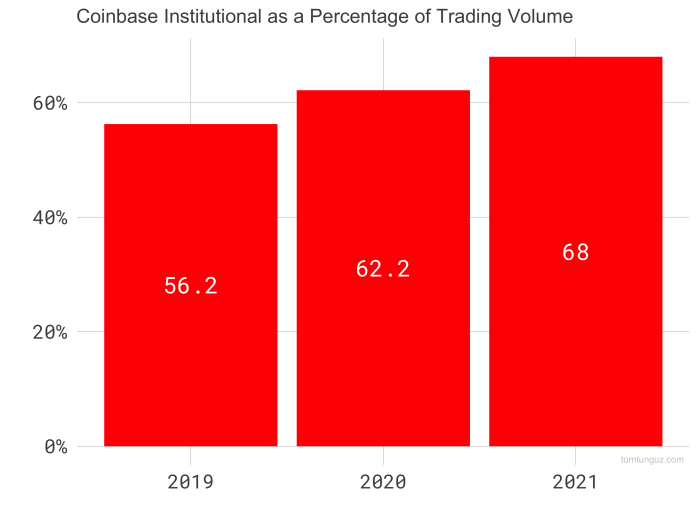

Institutional investors’ share of trading volume on Coinbase increased from 56.2% to 68.0% in 2 years. Institutional buyers typically trade larger volumes than retail investors, explaining some of the delta. The converse may be true for Uniswap: perhaps crypto whales (retail investors with significant balances) dominated the volume in 2020, and to a lesser extent in 2021.

Last, COIN and UNI are different instruments. COIN is a stock. UNI is a governance token. Stock affords the holder rights to future dividends and voting power on company matters. UNI affords its holders a vote, but not a dividend right. This could change in the future.

So, should COIN and UNI trade at the same multiple?

Uniswap grows MTUs faster, likely generates significantly more profit, and has fallen less. But revenue growth is more sensitive to market swings, the company discloses fewer operating metrics, and their token offers fewer rights than COIN stock.

If an investor values profit margin over dividend rights, then yes. But if the UNI token never offers a dividend, then no.

The answer isn’t clear today. We need standardized reporting for tokens and equivalent shareholder rights to compare equities to tokens: an essential step to enticing more investment in web3.

Thanks to my partner Urvashi Barooah for inspiring this post!