NPS is a retirement product. Specifically targeted to accumulate funds for retirement.

Here is how NPS can help you accumulate funds for retirement.

- You accumulate money until you retire.

- You withdraw from the corpus after you retire.

- You can invest your money in a diversified portfolio of equity and debt.

- You can withdraw a portion lumpsum and use the rest the purchase an annuity plan. The annuity plan can provide you with an income stream during retirement.

But you can do all the above (and more) with mutual funds too, right?

- You can invest in MFs while you are working.

- You can start withdrawing from MFs once you retire.

- You can take exposure to different assets through mutual funds too.

- And nobody stops you from buying an annuity plan using your MF portfolio whenever you want.

Both NPS and mutual funds are market-linked products. Your money is managed by professional money managers and your returns will depend on the performance of your funds.

In that case, which is a better vehicle to accumulate your retirement corpus? NPS or mutual funds?

In this post, let us compare NPS and mutual funds on various aspects and consider various nuances of these investments.

Note: NPS and mutual funds are NOT only investments for retirement. There are many others too and such investments can be part of your retirement portfolio too. However, in this post, we limit the analysis to NPS and mutual funds.

#1 NPS vs Mutual funds: Type of investment

Both are market linked investments.

No guarantee of returns.

With NPS, you can split your money across Equity Fund (E), Government bonds (G), and Corporate Bonds (C). There is Asset Class A too, where you get exposure to alternative assets like REITs, INVITs, AIFs, etc.

You can select Active choice, where you decide the allocation to various asset classes or funds (E,C,G A). Maximum equity allocation can be 75%. Maximum allocation to A can be 5%.

OR

You can opt for Auto-choice. Choose from 3 life cycle funds (Aggressive, Moderate, Conservative). In the lifecycle funds, the allocation to E, C, and G funds is pre-defined as per a matrix, and the risk in the portfolio (exposure to E) goes down with age. Portfolio rebalancing also happens automatically in the auto-choice lifecycle funds.

With mutual funds, there is no dearth of choice. You have several types of equity and debt funds. You can invest even in gold, silver, and even foreign equities. You can decide asset allocation and choose funds freely.

#2 NPS vs Mutual Funds: Exit Rules

NPS is quite strict here. Expected too from a retirement product.

In NPS, you cannot exit before attaining the age of 60. Hence, your money is virtually locked in until the age of 60.

Point to Note: There is no requirement that you must exit NPS when you turn 60. The NPS rules allow you to defer the exit from NPS until the age of 75.

At the time of exit, you can withdraw up to 60% of the accumulated corpus as lumpsum. You must utilize the remaining 40% to purchase an annuity plan. However, if you wish, you can even utilize the entire amount to purchase an annuity plan. 0-60% lumpsum withdrawal. 40-100% annuity purchase.

Yes, you can exit NPS prematurely too once you complete 10 years. However, for pre-mature exit, you must use 80% of the accumulated corpus to purchase an annuity plan. Only 20% can be taken out lumpsum. NPS also permits partial withdrawals in certain situations.

With mutual funds, there is no restriction on exit from any scheme. You can sell whenever you want. The only exception is ELSS where your investment is locked in for 3 years from the date of investment.

In case of NPS, annuity purchase will happen with pre-tax money.

You can purchase annuity plans using your MF proceeds too. However, please understand, in case of mutual funds, annuity purchase will happen with post-tax money. You will sell your mutual funds to buy an annuity plan and sale of MFs will result in capital gains liability.

#3 NPS vs Mutual Funds: Tax-Treatment on Investment

Own Contribution to NPS account

If you are filing ITR under Old tax regime, you will get tax benefit under Section 80CCD(1B) for up to Rs 50,000 per financial year for investment in Tier-1 NPS. This tax benefit is available over and above tax benefit of Rs 1.5 lacs under Section 80C.

Benefit under Section 80CCD(1B) not available under New Tax Regime.

Employer contribution to NPS account

This is applicable to only salaried employees. And even there, not all employers offer this. However, if your employer offers NPS, you can save some serious tax if your employer offers to contribute to your NPS account.

Employer contribution to your NPS, EPF, and superannuation account is exempt from tax upto Rs 7.5 lacs per annum. For NPS, this tax exemption has an additional cap. Such a contribution must not exceed 10% of basic salary. The cap increases to 14% for state and central Government employees.

In this post, whenever I refer to NPS, I mean Tier-1 NPS. There is NPS-Tier 2 as well and you can get tax-benefit for investment in Tier-2 NPS subject to conditions. However, I have not considered Tier-2 NPS here because it is not a pure retirement product. Additionally, I am referring to All Citizens Model or Corporate NPS model.

In case of mutual funds, there is no tax benefit on investment, except for ELSS. Investment in ELSS qualifies for tax benefit under Section 80C of the Income Tax Act.

#4 NPS vs Mutual Funds: Tax Treatment on Exit

NPS: At the time of exit, any lumpsum withdrawal (up to 60% of the accumulated corpus) is exempt from income tax.

Remaining amount (40%) must be used to purchase an annuity plan. While this amount used to purchase annuity plan is not taxed, the payout from an annuity plan is added to your income and taxed at your slab rate.

Mutual fund taxation depends on the type of mutual fund and the underlying domestic equity exposure.

#5 NPS vs Mutual Funds: NPS allows tax-free rebalancing

NPS wins this contest easily. Tax-free rebalancing is the biggest positive of NPS.

In NPS, taxes come into picture only at the time of exit from NPS. Not before that. Hence, your money can compound unhindered by the friction of taxes.

Switching money between different types of funds or even switching to a different pension fund manager does not result in any capital gains. Hence, no capital gains taxes.

This makes portfolio rebalancing super tax-efficient.

So, let us say your NPS portfolio is 50 lacs. Active-choice NPS.

Rs 30 lacs in E and a cumulative 20 lacs in E and G.

Your target allocation is 50:50 Equity: debt but it has gone to 60:40 equity: debt because of the stock market run-up. You can simply tweak your allocation to E:C: G slightly (to say 51:25:24) and the portfolio will rebalance to your target level (quite close to that). You will not have to pay any taxes during rebalancing in NPS.

In Auto-choice NPS, rebalancing happens automatically on your birthday. In Active choice, you must do this manually.

This is important considering the taxation of mutual fund investments has become increasingly adverse over the past decade.

2015: Long-term holding period for debt funds was increased from 1 year to 3 years. Not as much of a problem.

2018: Long-term capital gains tax brought in for equity funds. Any LTCG on sale of stocks/equity MF more than Rs 1 lac in a financial year taxed at 10%.

2023: Concept of long-term capital gains removed from debt funds. For debt MF units bought after March 31, 2023, all capital gains arising out of sale of such units shall be considered short term gains and be taxed at income tax slab rate (marginal tax rate). This is the biggest problem.

Clearly, if you must rebalance a portfolio of mutual funds, there will be leakage in the form of taxes. This will hinder compounding. Moreover, it is not just about rebalancing. You may have invested in a mutual fund that you do not like as much anymore. In absence of taxes, you would simply switch to the mutual fund that you like more. However, taxes make this entire exercise difficult.

For rebalancing, there is a small workaround that you can use in some cases. Instead of shuffling old investments, tweak the incremental allocation. For instance, let us say your target equity: debt allocation is 50:50. Because of the recent market fall, the asset allocation is now 45:55 equity: debt. You can route all incremental cashflows to equity funds until the asset allocation shifts back to target allocation. Since you are not selling anything there is no problem of taxes. Personally, I find this much approach a bit cumbersome and difficult to execute. This approach will anyways not work for bigger portfolios.

#6 NPS vs Mutual Funds: Early retirement can be a problem

What if you decide to retire at the age of 55 and not 60?

NPS is rigid. Retirement means 60 and above.

Hence, if you opt for an early retirement and most of your retirement money is in NPS, you have a problem.

If you exit at the age of 55, then you must use 80% of the accumulated corpus towards purchase of an annuity plan.

Note that NPS account does not have to closed when you stop working. You can continue the account even beyond your retirement. Hence, even if you were to retire at 55, you can continue and even contribute to your NPS account until the age of 60,70, or 75.

With mutual funds, you will NOT face this problem. You can take out your money whenever you want. Withdrawals are not linked to your age.

On a side note, while NPS may trail MFs in flexibility, it is far ahead of other pension products.

I am comparing NPS to pension products from life insurance companies in India. Life insurance companies have launched pension products in both linked and non-linked variants.

In NPS, your investments do not have to be systematic. You can even make big lumpsum investments. No limits. With other pension products, you must pay a certain amount of premium every year. Topping up is not easy.

Proceeds from ULIPs (with annual premium > 2.5 lacs) and Traditional plans (with annual premium > 5 lacs) are now taxable. No such problem with NPS.

In NPS, you can withdraw 60% of accumulated corpus tax-free. In pension plans from insurance companies, you can withdraw only 1/3rd of accumulate corpus tax-free.

#7 NPS vs Mutual Funds: NPS has lesser choice

You can invest in only 1 equity fund under NPS. Likewise for C and G funds.

While your Equity(E), Government bonds (G), and Corporate Bonds (C) can be from different pension fund managers, you still have just 1 equity fund in your NPS portfolio. 1 actively managed equity fund. I would expect these equity funds from NPS to have a large-cap tilt.

Each Pension fund manager (PFM) offers 1 E, 1 G, and 1 C fund. You can invest in only 1 E, G, and C funds. From the same or different PFMs. You cannot invest in 2 equity funds. Or equity funds from 2 pension fund managers.

Mutual funds offer a much wider variety of choices. You have large cap, midcap, and small cap funds. Both active and passive. Flexicap, Factor, Sectoral, Thematic. Foreign equity. You name it and you have it.

When it comes to investments, less choice is not necessarily bad. However, most investors would not want to keep all their equity money in a single actively managed fund, as is the case in NPS.

#8 NPS vs Mutual Funds: Returns

I do not want to compare returns. Simply because NPS funds have much lesser restrictions on where they can invest. What should be the true benchmark for an NPS Equity fund? Nifty 50, Nifty 100, Nifty 500? Which equity mutual funds should I compare the performance with?

You can check the returns of various NPS schemes here.

#9 NPS vs Mutual Funds: Costs

NPS is the lowest cost investment product. The Investment management fee is less than 10 bps.

Mutual funds expenses are much higher. Depends on multiple factors. Regular or Direct. Equity or Debt. Active or Passive.

#10 NPS vs Mutual Funds: Is mandatory annuity purchase a problem?

With an annuity plan, you pay a lump sum to the insurance company. And the insurance company guarantees you an income stream for life.

Mandatory annuity purchase has been highlighted a major problem of NPS.

However, I do not see mandatory annuity purchase as a problem. Any good retirement product should have the facility to divert an allocation towards annuity purchase. However, you must buy the right variant at the right age.

Yes, if you are smart with money, you can manage without an annuity plan. However, most investors would struggle to generate regular cashflows during retirement from a market linked portfolio. If payouts from an annuity plan can cover a portion of your expenses, I do not see much problem there.

Even if you are smart, you must consider following points.

- With annuity plans, you can lock-in interest rate for life. No other product can do this. Yes, there are long term Government Bonds with maturity of up to 40 years. Still not for life. Only annuity products can. What if

- Covers longevity risk. The income will continue for life. Even if the amount is small, you will never run out of money. Can buy variants where your spouse will receive money after you. These are practical life situations that need to be provided for. Not everyone in the family can manage withdrawals from a diversified portfolio.

- By staggering annuity purchases can increase income and reduce risk in the portfolio. By ensuring a basic level of income, you can take higher risk (commensurate with your risk profile) with your remaining investments and potentially earn better returns.

It is not an either-or decision

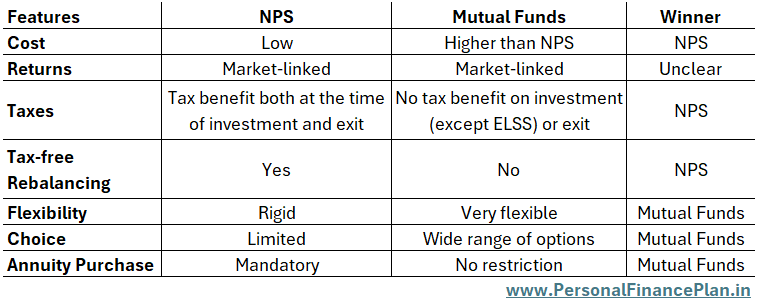

A quick comparison on all the aspects we discussed above.

- Cost: NPS wins here.

- Returns: Both are market-linked. I prefer NOT to compare returns.

- Taxes: NPS wins here, both in tax benefit on investment and tax treatment at the time of exit.

- Flexibility: Mutual funds win here. No lock-ins. Easy withdrawals. Exit not linked to age. NPS is rigid.

- Choice: Mutual funds are a clear winner. Far greater choice of funds compared to NPS.

- Mandatory Annuity Purchase: NPS has this restriction. Mutual funds do not. I do not see mandatory annuity purchase as a problem. With mutual funds too, you can buy an annuity plan.

Note: In case of NPS, annuity purchase will happen with pre-tax money. In case of mutual funds, annuity purchase will happen with post-tax money.

So, which is a better investment vehicle for retirement savings? MFs or NPS?

I do not think we have an objective winner here. There are areas where NPS fares better. And there are aspects where MFs win. Depends on your requirements.

Moreover, it is not an either-or decision. You can use both.

When you are planning for retirement, you do not have to keep all your retirement money in a single vehicle. You can use multiple vehicles for the same goal.

Hence, you can invest in both mutual funds and NPS for your retirement.

If the rigid exit rules or the lack of choice of funds in NPS worries you, you can invest more in mutual funds.

If tax-free rebalancing is a high priority, you can allocate a sizeable amount in NPS.

Yes, you can have other products too in your portfolio such as EPF, PPF, Gold, bonds etc). For this post, I am limiting discussion to MFs and NPS.

An example of how you can benefit from tax-free rebalancing feature of NPS.

Let us say, for your retirement portfolio, you have Rs 40 lacs in NPS and Rs 40 lacs in mutual funds.

NPS: E: 24 lacs, G: 8 lacs C: 8 lacs

Mutual funds: Equity Funds: 28 lacs, debt funds: 12 lacs

Total equity allocation = 24 + 28 = Rs 52 lacs, which is 65% allocation to equities.

But you wanted 60:40.

If you sell equity funds and buy debt funds, you will have to pay tax.

On the other hand, if you could shift Rs 4 lacs from NPS-Equity (E) fund to G and C funds, we can go to back to 60:40 target allocation without paying any taxes. And you can do that by simply changing asset allocation in NPS to 50:25:25 (E:G:C).

Personally, I prefer to have the bulk of the money in mutual funds. Greater choice of funds. Availability of passive investments. Better disclosures than NPS funds. More focused regulator (SEBI vs. PFRDA). At the same time, having a decent allocation to NPS would not harm because of the tax-free rebalancing feature. In fact, the allocation to NPS can come in handy since you can purchase an annuity plan from pre-tax money after you retire.

What do YOU prefer for your retirement savings: NPS or Mutual funds?

Image Credit: Unsplash

Disclaimer: Registration granted by SEBI, membership of BASL, and certification from NISM in no way guarantee performance of the intermediary or provide any assurance of returns to investors. Investment in securities market is subject to market risks. Read all the related documents carefully before investing.

This post is for education purpose alone and is NOT investment advice. This is not a recommendation to invest or NOT invest in any product. The securities, instruments, or indices quoted are for illustration only and are not recommendatory. My views may be biased, and I may choose not to focus on aspects that you consider important. Your financial goals may be different. You may have a different risk profile. You may be in a different life stage than I am in. Hence, you must NOT base your investment decisions based on my writings. There is no one-size-fits-all solution in investments. What may be a good investment for certain investors may NOT be good for others. And vice versa. Therefore, read and understand the product terms and conditions and consider your risk profile, requirements, and suitability before investing in any investment product or following an investment approach.