The VantageScore model offers these advantages to lenders and consumers:

- It was developed by the three major credit bureaus to offer a model across all bureaus that’s more consistent than FICO.

- It calculates scores for more people by giving a score to people with a shorter credit history.

Both models are consistent enough that knowing where you stand in one gives you a reliable indication of your credit in general.

What Makes a Good Credit Score?

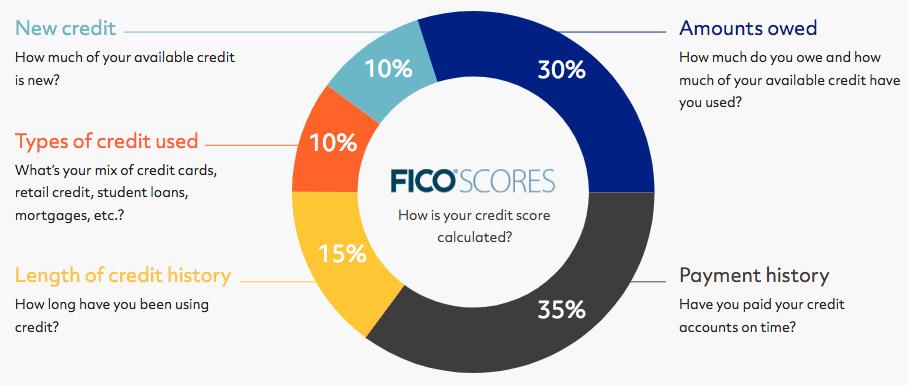

The same primary considerations go into calculating VantageScore credit scores and FICO credit scores:

-

- Payment history

- Credit utilization

- Credit age

- Mix of accounts

- New credit inquiries

Payment History

A history of late and missed payments for either scoring model lowers your credit score more than any other factor.

When determining your score, the FICO and VantageScore scoring models look at how recently you missed a payment or were late, how many accounts you were late on, and how many total payments on each account were missing or late.

Credit Utilization Ratio

Your credit utilization ratio is the amount of credit you’ve used divided by your total available credit limit. For example, if you have credit cards with a combined credit limit of $8,000 and balances of $3,000, your credit utilization ratio is 37.5%.

A good credit score requires a credit utilization ratio of 30% or less, although 10% or less is ideal.

Credit Age

Your credit age is how long you’ve used credit. More specifically, the length of your credit history is how long your credit accounts have been reported open, and your credit age is the average of how long all of your accounts have been open.

Say your oldest account was closed and fell off your file, and the next oldest account is 10 years “younger” than the account that fell off. Now, instead of showing how long you’ve actually used credit overall, credit files may show the age of the oldest account on file and your score may decrease.

To maintain a high credit age, keep at least one account on your credit file that is at least six months old. As you grow older, it should be easier to maintain a higher credit score as your accounts continue to grow in credit age.

Account Mix

Account mix is how many installment accounts and revolving accounts you have.

- Installment accounts are loans—such as mortgages, car loans, or personal loans—with a fixed monthly payment for a specific term (number of months or years).

- Revolving accounts are credit cards and credit lines with a credit limit that you can charge against.

Lenders want to see you can handle both types of accounts, so a good mix of the two makes for a better credit score.

Credit Inquiries

Hard inquiries happen when a lender looks at your credit report because you’ve applied for credit. A hard inquiry affects your credit score—lowering it by 5 to 10 points. The inquiry can stay on your credit report for up to two years, but it will impact your score for only 12 months. Though hard inquiries make up only 10% of your score, try to minimize credit inquiries to maximize your score.

When you need an auto loan or mortgage, it’s normal to shop around to find the best rates. Depending on the scoring model used, if you do your loan shopping in a 14- to 45-day span, the inquiries can be lumped into a single inquiry and affect your score less. FICO score models allow 45 days. On the other hand, the VantageScore model uses only a 14-day span.

Soft inquiries, such as SparkRental tenant credit reports use, don’t affect your credit score.